Retail

The evolution of private label: from cheaper alternative to prime differentiator

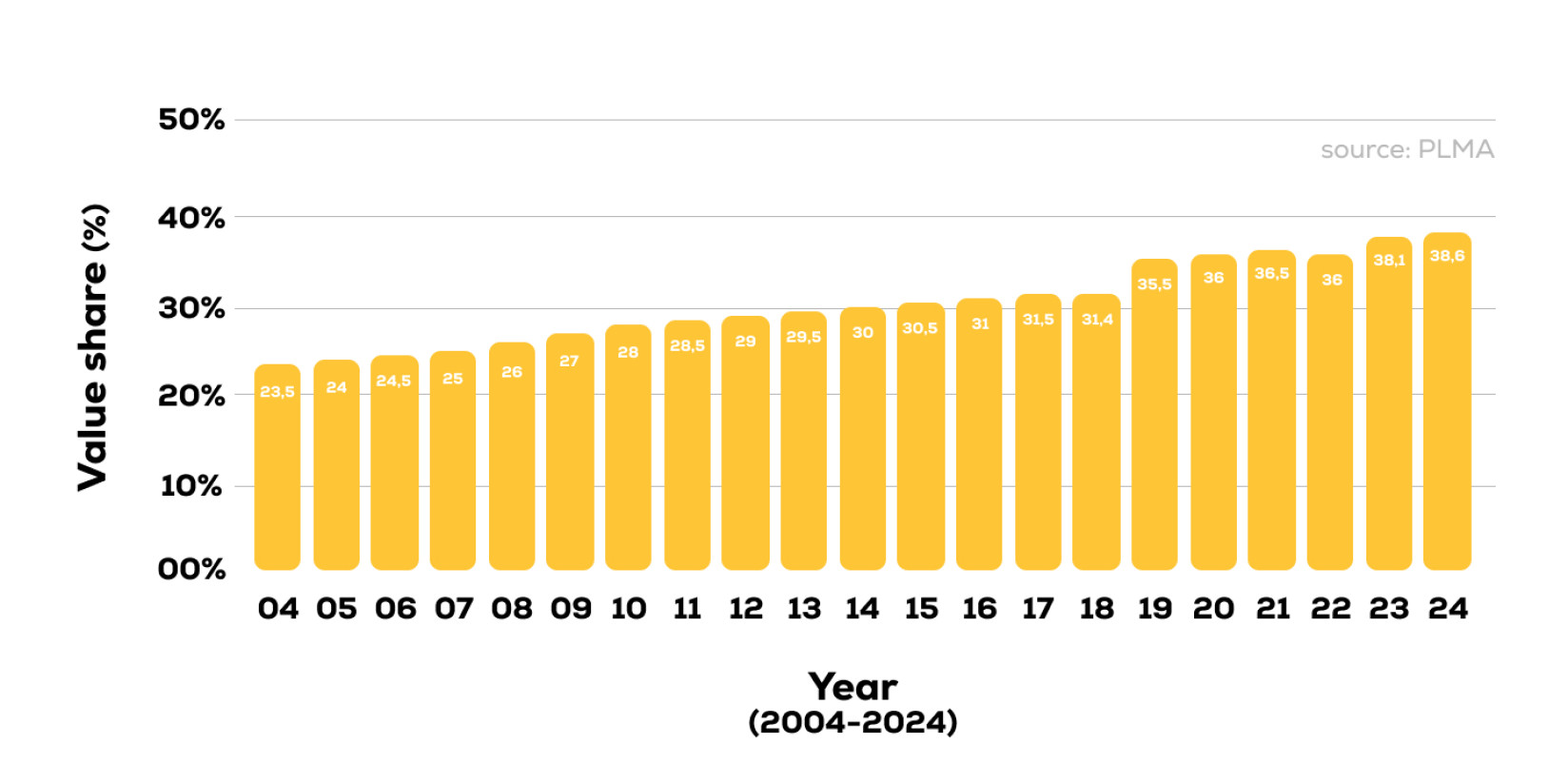

Private label today continues to thrive and grow. In the European markets we see private label taking around 38.1% market share, while it’s reaching the 20% mark in the US market. A shift in strategy and economic developments keep fueling its success. Back in the earlier years, private label was a whole different ball game. Let’s dive into the history of private label.